The Connection Between Financial Stress and Mental Health

Amid a cost-of-living crisis, everyday money worries can compound, resulting in significant stress for many Canadians. Nearly half of Canadians, or 48 per cent, say

Amid a cost-of-living crisis, everyday money worries can compound, resulting in significant stress for many Canadians. Nearly half of Canadians, or 48 per cent, say

Living in Canada is more expensive than ever. Rampant inflation rates, dramatic mortgage rate hikes, and a crippling housing crisis are contributing to record-breaking amounts

Your wedding is likely to be one of the most memorable and exciting days of your life, so it’s no wonder you want it to

Payday loans are short-term loans usually up to $1,500 that can help individuals get through a rough spot. They are called payday loans because typically, they are paid

Payday loans are short-term loans usually up to $1,500 that can help individuals get through a rough spot. They are called payday loans because typically, they are paid

Payday loans are short-term loans usually up to $1,500 that can help individuals get through a rough spot. They are called payday loans because typically, they are paid

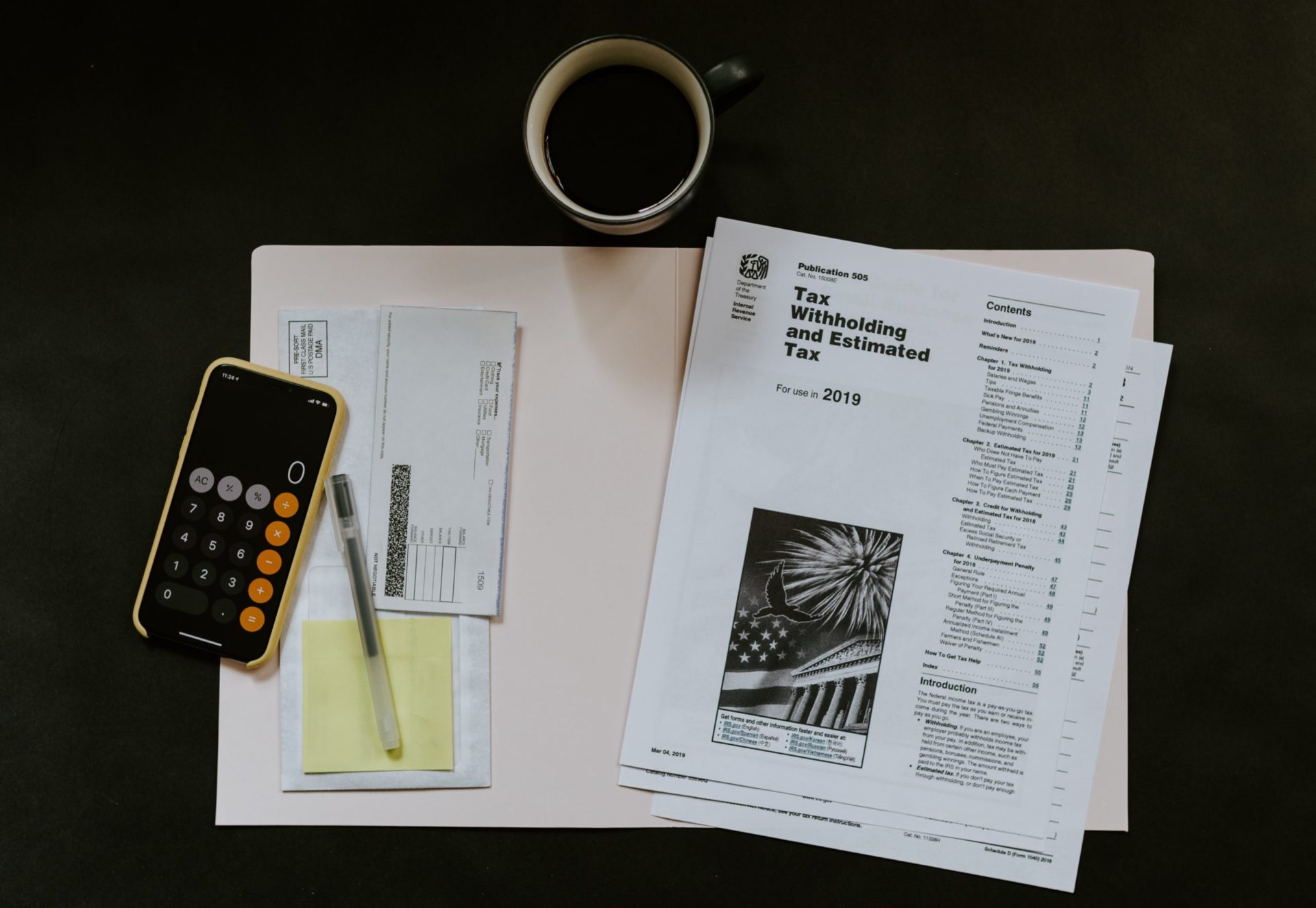

Spring is in bloom, which means that Canadians are preparing to file their annual tax returns. Most people are hoping for a refund, however statistics

In the Canadian housing market, it’s hard to buy a home without having a substantial down payment. As of January 2024, the average price of a

Fraud can affect people from all walks of life, regardless of their age, race, education levels or economic background. Both individuals and businesses are commonly

Considering various payment options to finance purchases might be extra appealing in this costly economy. One such service – buy now, pay later (BNPL) –